FX Weekly Overview: Key Events of the Week

- Bearish Factors

- A sharp acceleration of the IPCA-15 could solidify expectations for strong increases in the basic interest rate (Selic), which helps attract foreign investment and tends to strengthen the real.

- Bullish Factors

- Uncertainties regarding the application of import tariffs by the US government and the peace negotiation process between Russia and Ukraine could lead to increased risk aversion, which tends to strengthen the dollar globally.

- The PCE Index may reinforce the perception of more persistent inflation in the US, potentially increasing bets that American interest rates will remain high for longer, strengthening the dollar globally.

The week in review

The week was marked by volatility in currency markets, amid new import tariff threats by US President Donald Trump and geopolitical tensions after the US and Russia met to discuss the Ukraine conflict without its participation.

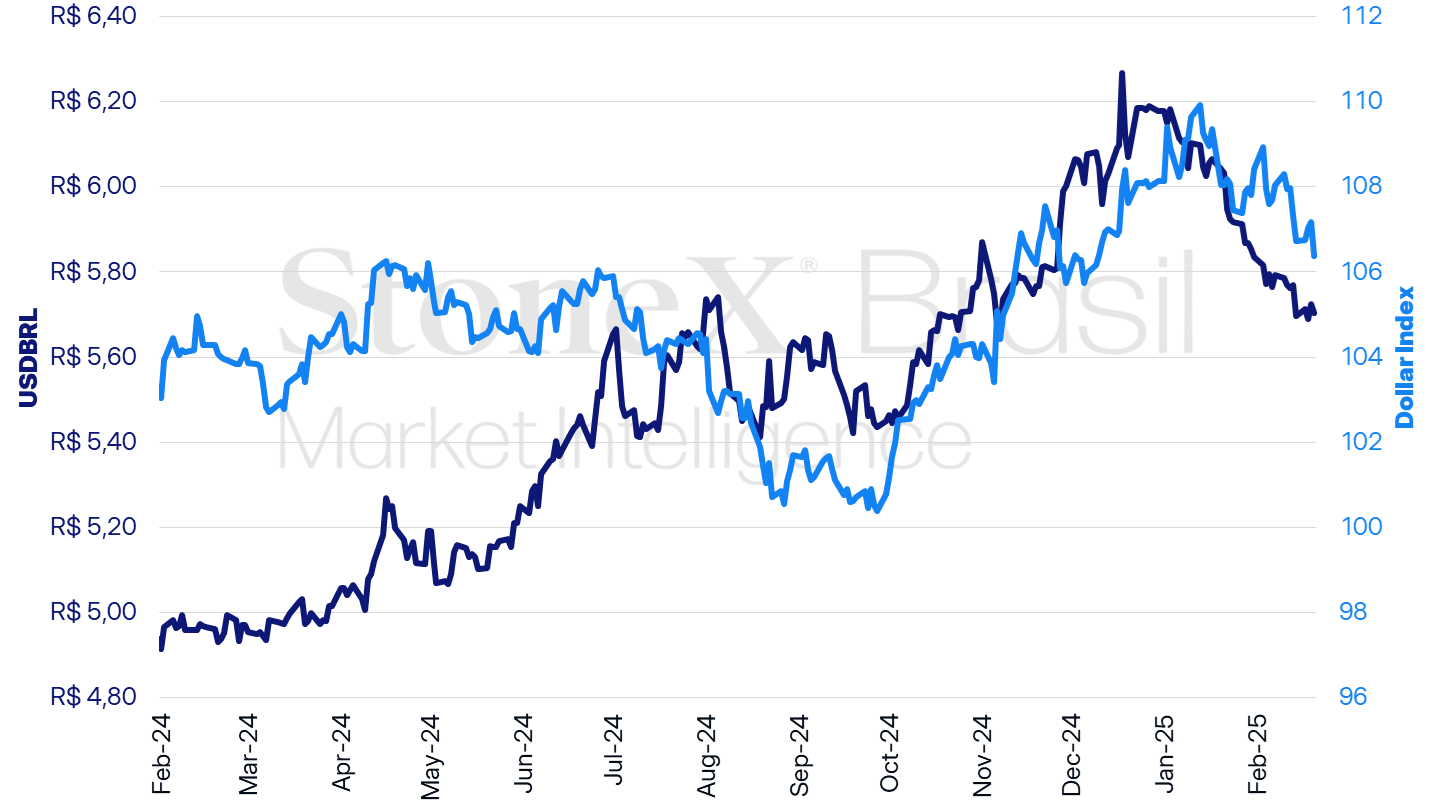

The USDBRL ended Friday’s (21st) session at BRL 5.7302, with a +0.6% variation for the week, -1.8% for the month, and -7.2% for the year. Meanwhile, the Dollar Index closed Friday’s session at 106.6 points, with a weekly decline of 0.1%, a monthly drop of 1.7%, and a yearly decrease of 1.4%.

USD/BRL and Dollar Index (points)

Source: StoneX cmdtyView. Design: StoneX.

KEY EVENT: Volatility and Unpredictability of the US Under Trump

Expected Impact on USDBRL: Bullish

In recent weeks, the perception that US President Donald Trump is taking a softer stance than anticipated on the application of import tariffs on other economies has led to broad weakening of the US dollar. Investors interpret Trump’s tariff threats as a negotiation tool to obtain concessions from other countries on key issues for the new administration, not necessarily linked to trade relations. For this reason, last week’s threats of imposing approximately 25% tariffs on imports of automobiles, semiconductors, pharmaceuticals, wood, and forest products starting in April had little effect on investors, who seem to believe these tariffs will be eased, restricted, or suspended before taking effect. Nonetheless, high uncertainty remains regarding the evolution of US trade policy in the coming weeks, and at least some of these tariffs are likely to be implemented, which tends to negatively impact risky assets such as stocks, commodities, and emerging market currencies.

Additionally, Donald Trump's government heightened geopolitical risk perceptions last week due to tensions and conflicts with allies in handling peace negotiations between Russia and Ukraine. First, high-level diplomats from Russia and the US met in Saudi Arabia to discuss the issue without Ukraine’s participation and without informing key allied leaders, such as those in Europe. Subsequently, the US president accused Ukraine of starting the war, labeled its president, Volodymyr Zelensky, as a “dictator without elections,” and stated that he “does not consider it very important that [Zelensky] be present at the negotiations [for peace]” because “he has done a terrible job negotiating so far.” Investors perceive that the US is attempting to force Ukraine into accepting a rushed deal, which increases concerns about the geopolitical stability of such a Washington-led agreement. This, in turn, favors safe-haven assets such as the US dollar.

US Inflation

Expected Impact on USDBRL: Bullish

The median forecast for the Personal Consumption Expenditures (PCE) Price Index indicates a 0.3% increase in January, repeating December’s increase, for both the headline and core index (which excludes volatile food and energy components), which had previously risen 0.2% in December. If these projections hold, they would reinforce the perception that US inflation remained elevated in January, potentially signaling the end of price stabilization efforts in the country. However, since the COVID-19 pandemic, US inflation has shown stronger seasonal pressures in Q1 of each year, an effect that has not persisted into later months. Thus, investors may refrain from reacting strongly to this data and instead wait for additional indicators to provide a clearer macroeconomic outlook for 2025, particularly given the mixed signals observed in January.

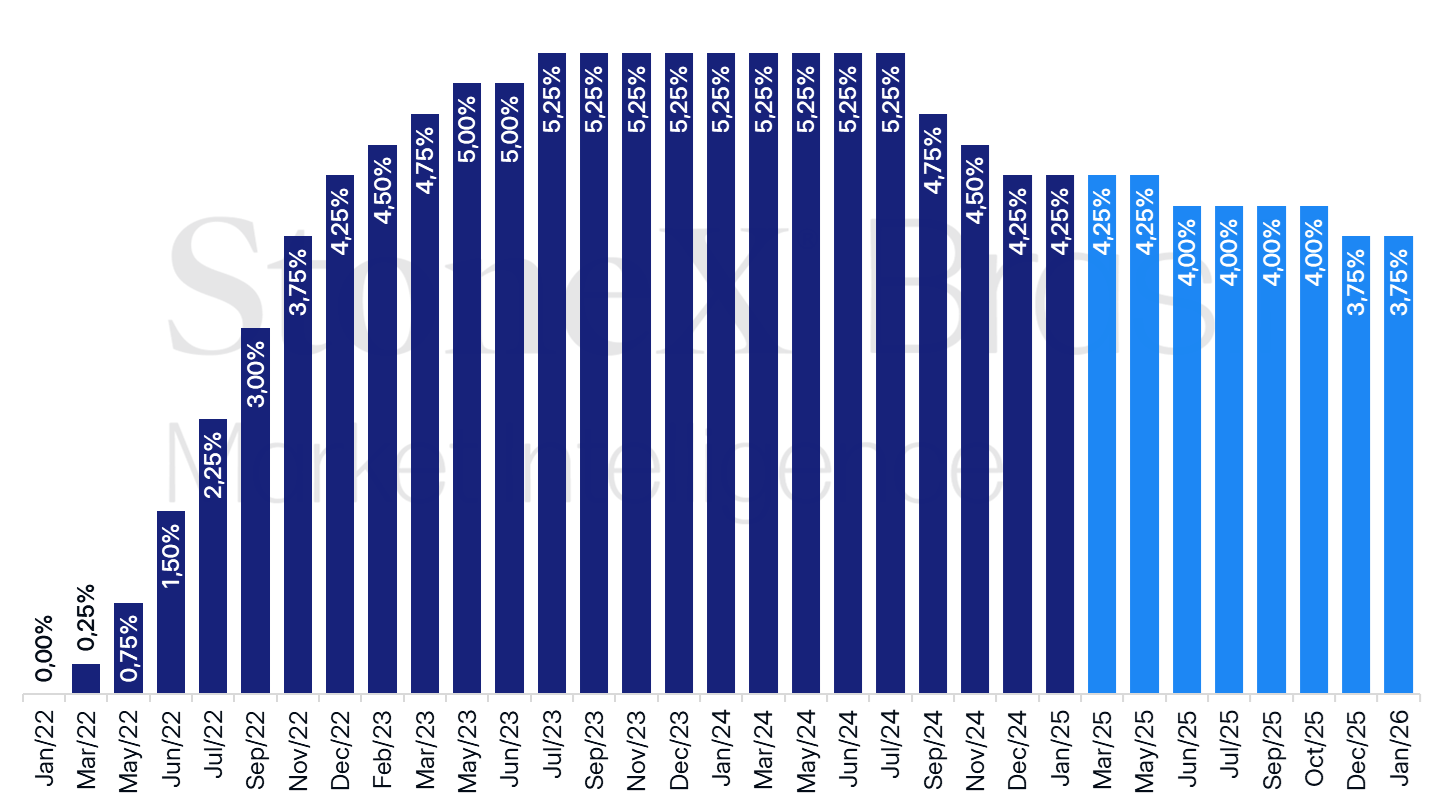

US: Historical and Expected Interest Rate Path – February 21, 2025

Source: CME FedWatch Tool. Design: StoneX. (Represents the most probable futures market bet for interest rates on the specified date.)

IPCA-15 and Employment Data in Brazil

Expected Impact on USDBRL: Bearish

In Brazil, the highlight of the week will be the Consumer Price Index – 15 (IPCA-15) for February, which has a median forecast of a 1.38% increase—a significant acceleration compared to the 0.11% increase recorded in January. However, last month’s moderate reading was partially influenced by one-off factors, particularly the “Itaipu energy bonus”. The 0.67% rise in the core index (excluding volatile food and energy components) and the 0.81% increase in service prices had already pointed to stronger inflationary pressures in January. Therefore, if the February forecast is confirmed, the IPCA-15 could worsen inflation expectations for 2025 and reinforce the outlook for higher Selic interest rates. This, in turn, enhances the profitability of Brazilian bonds, potentially attracting foreign capital and strengthening the real.

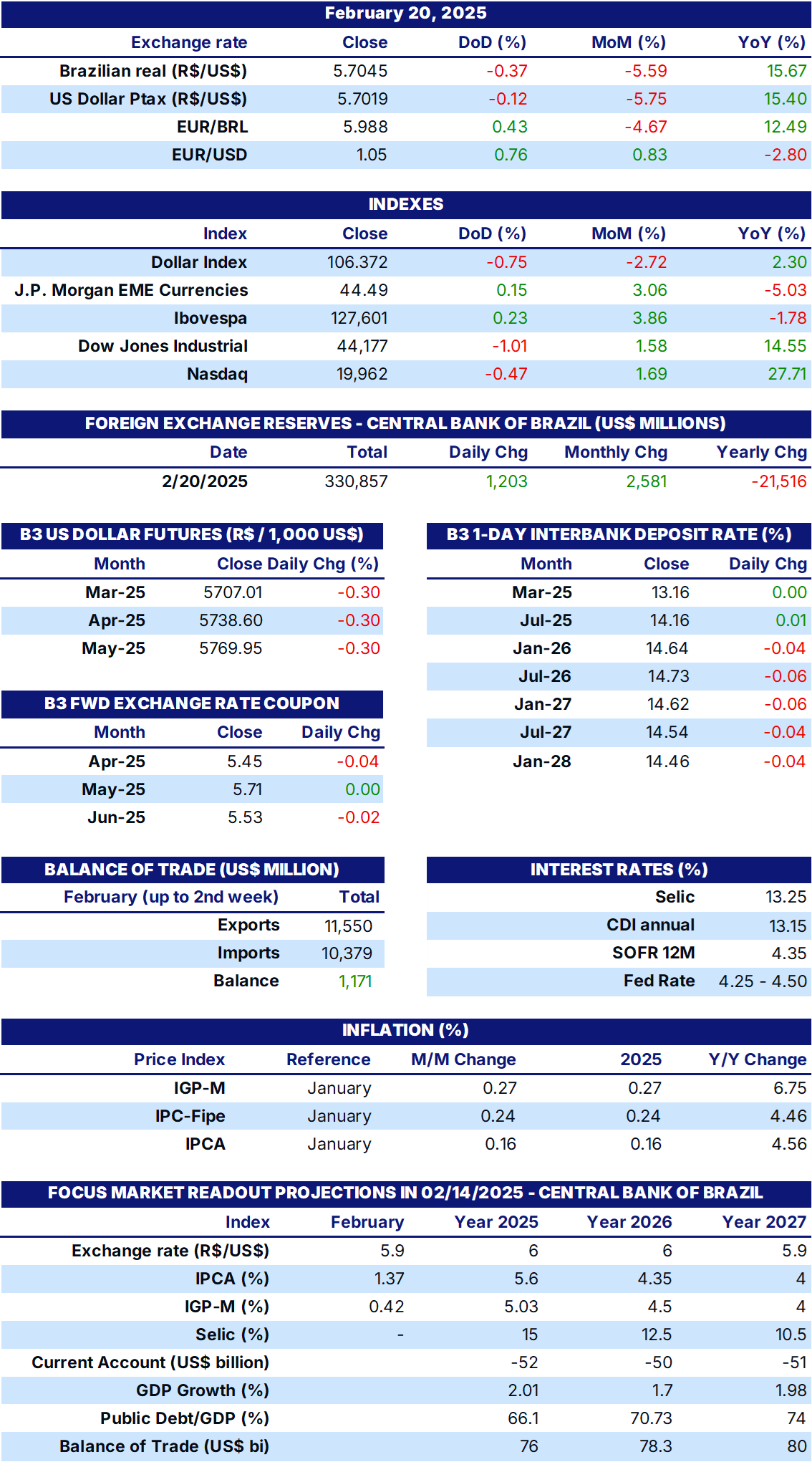

INDICATORS

Sources: Central Bank of Brazil; B3; IBGE; Fipe; FGV; MDIC; IPEA; and StoneX cmdtyView.

The StoneX Group Inc. group of companies provides financial services worldwide through its subsidiaries, including physical commodities, securities, exchange-traded and over-the-counter derivatives, risk management, global payments and foreign exchange products in accordance with applicable law in the jurisdictions where services are provided. References to over-the-counter (“OTC”) products or swaps are made on behalf of StoneX Markets LLC (“SXM”), a member of the National Futures Association (“NFA”) and provisionally registered with the U.S. Commodity Futures Trading Commission (“CFTC”) as a swap dealer. SXM’s products are designed only for individuals or firms who qualify under CFTC rules as an ‘Eligible Contract Participant’ (“ECP”) and who have been accepted as customers of SXM. StoneX Financial Inc. (“SFI”) is a member of FINRA/NFA/SIPC and registered with the MSRB. SFI is registered with the U.S. Securities and Exchange Commission (“SEC”) as a Broker-Dealer and with the CFTC as a Futures Commission Merchant and Commodity Trading Adviser. References to securities trading are made on behalf of the BD Division of SFI and are intended only for an audience of institutional clients as defined by FINRA Rule 4512(c). References to exchange-traded futures and options are made on behalf of the FCM Division of SFI . StoneX is a trading name of StoneX Financial Ltd (“SFL”). SFL is registered in England and Wales, Company No. 5616586. SFL is authorized and regulated by the Financial Conduct Authority [FRN 446717] to provide to professional and eligible customers including: arrangement, execution and, where required, clearing derivative transactions in exchange traded futures and options. SFL is also authorised to engage in the arrangement and execution of transactions in certain OTC products, certain securities trading, precious metals trading and payment services to eligible customers. SFL is authorised & regulated by the Financial Conduct Authority under the Payment Services Regulations 2017 for the provision of payment services. SFL is a category 1 ring-dealing member of the London Metal Exchange. In addition SFL also engages in other physically delivered commodities business and other general business activities which are unregulated and not required to be authorised by the Financial Conduct Authority. StoneX Group Inc. acts as agent for SFL in New York with respect to its payments services business. StoneX APAC Pte. Ltd. acts as agent for SFL in Singapore with respect to its payments services business. ‘StoneX’ is the trade name used by StoneX Group Inc. and all its associated entities and subsidiaries.

Trading swaps and over-the-counter derivatives, exchange-traded derivatives and options and securities involves substantial risk and is not suitable for all investors. Past performance of any futures or option is not indicative of future success. Indicators are not a trading system and are not published as a specific trade recommendation. The information herein is not a recommendation to trade nor investment research or an offer to buy or sell any derivative or security. It does not take into account your particular investment objectives, financial situation or needs and does not create a binding obligation on any of the StoneX group of companies to enter into any transaction with you. You are advised to perform an independent investigation of any transaction to determine whether any transaction is suitable for you. No part of this material may be copied, photocopied or duplicated in any form by any means or redistributed without the prior written consent of StoneX Group Inc.

© 2025 StoneX Group Inc. All Rights Reserved.

Discover more insights